Key Takeaways

- The choice between direct oversight and a fund structure is a governance question — where authority, accountability, and decision rights reside.

- Fee layering in fund-of-funds structures compounds against net returns; each additional tier reduces the base on which future compounding occurs.

- Incentive misalignment between managers, fund vehicles, and allocators tends to surface most clearly under stress — not in stable markets.

- Clarity of decision authority reduces ambiguity when assumptions fail; direct oversight concentrates that authority where accountability sits.

- Governance is only meaningful if it is observable — documentation of credit parameters, IC approvals, and modification policies is the operational test.

Direct Oversight vs Fund Models: Why Decision Structure Matters

Institutional capital often focuses on manager selection, track record dispersion, and access. Those variables matter. But before evaluating managers, allocators confront a more structural question: what decision architecture governs their capital?

The comparison between direct oversight vs fund model is not primarily about performance marketing or access to deals. It is about where authority sits, how incentives compound, and how governance functions under stress.

This article evaluates the structural distinction across three lenses:

- Fee drag

- Incentive alignment

- Control and underwriting governance

The objective is not to critique fund models. Many operate responsibly and with integrity. The objective is to clarify how structure shapes outcomes, particularly when conditions deviate from base-case expectations.

Direct Oversight vs. Fund-of-Funds: Key Structural Differences

| Dimension | Direct Oversight | Fund-of-Funds / Third-Party |

|---|---|---|

| Fee structure | Single management layer; transparent costs | Multiple tiers at vehicle and manager level |

| Governance authority | Centralized; decision rights held by capital provider | Distributed; authority resides with underlying managers |

| Underwriting control | Credit box set and monitored at governing level | Underwriting delegated to individual fund managers |

| Alignment under stress | Single accountability chain; incentives are direct | Manager, fund, and allocator incentives may diverge |

| Reporting transparency | Cost attribution traceable to asset level | Attribution complexity increases across tiers |

| Best for | Allocators prioritizing governance clarity and accountability | Allocators prioritizing diversification, access, or specialization |

The Real Question Is Not “Which Fund Is Better?” — It Is “Where Does Control Live?”

Before comparing structures, definitions are necessary.

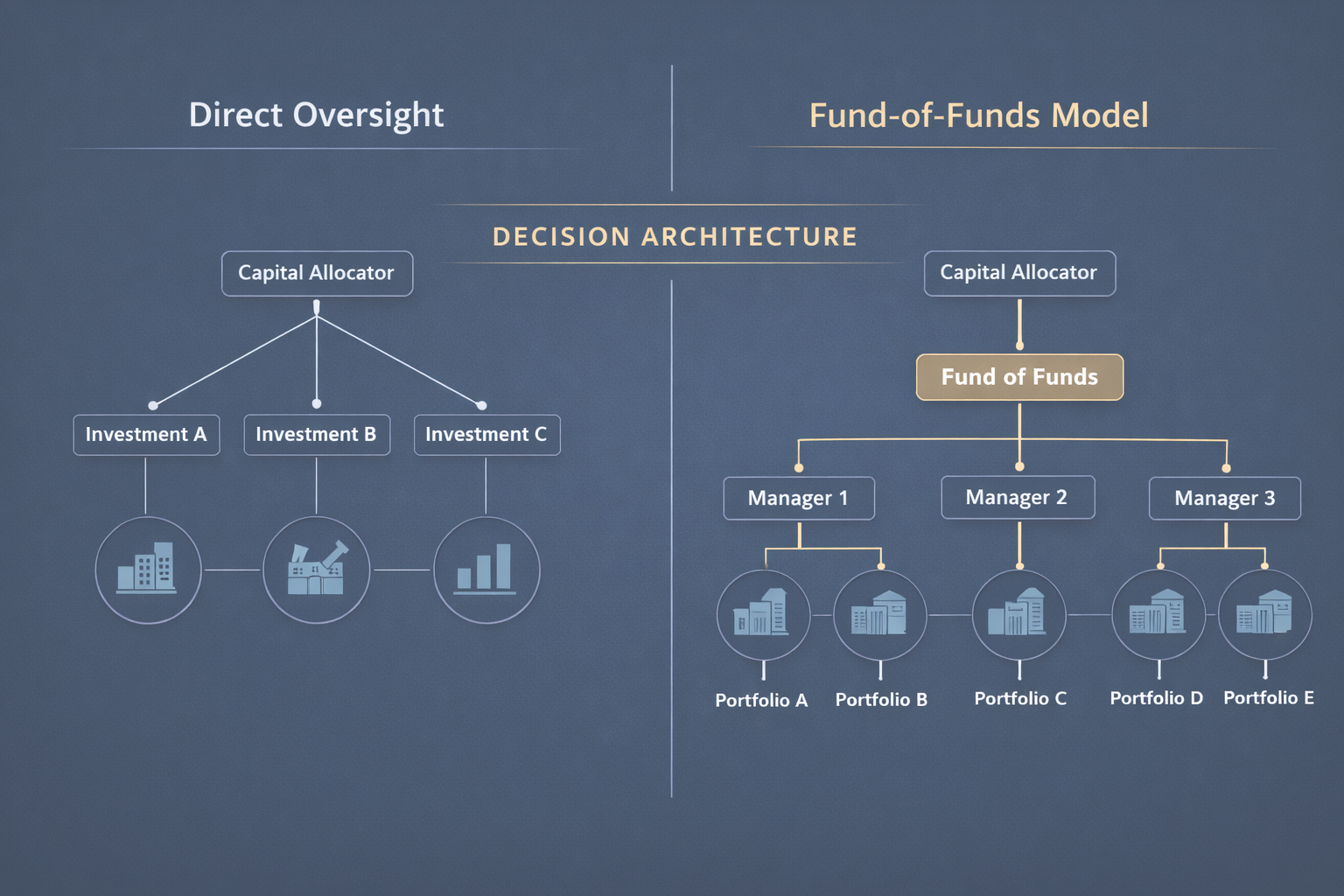

Direct Oversight Model

A direct oversight model is one in which the capital provider retains structural authority over underwriting standards, capital deployment decisions, and portfolio governance. Investment teams execute within a clearly defined mandate, but ultimate decision rights and policy frameworks remain centralized and transparent.

In this structure:

- Underwriting criteria are established and monitored at the top level.

- Sponsor selection and credit box parameters are explicitly defined.

Extension decisions, workouts, and restructuring policies follow documented governance protocols.

Fee arrangements are typically singular rather than layered.

The key characteristic is that discretion and governance sit close to capital.

Fund-of-Funds and Third-Party Fund Structures

A fund-of-funds structure allocates capital to underlying third-party managers. Capital flows through at least one intermediary vehicle before reaching the operating investment layer.

In this architecture:

- The allocator selects managers rather than individual investments.

- Underwriting authority resides with underlying managers.

- Performance and management fees may exist at multiple tiers.

Governance is indirect, often exercised through LP (limited partners) advisory committees rather than investment-level decision rights.

Again, this is not inherently inferior. It may offer diversification, specialization, and access benefits. The structural distinction is simply that control is distributed.

The question becomes: how does that distribution affect economics, incentives, and decision-making?

Lens #1 — Fee Drag: Why Layering Compounds Against the Allocator

Fees are not merely a line item. They are a structural input into compounding.

Management Fee Layering

In a direct oversight structure, there is typically a single management layer. Administrative expenses and operating costs are transparent within that structure.

In a fund-of-funds structure, management fees can exist at:

- The top-level vehicle

- Each underlying manager

- In some cases, operating-level asset management entities

Even if each layer appears reasonable in isolation, fee layering in private funds can compound against net returns over time.

A simplified way to think about it:

- A 1%–2% management fee at multiple tiers does not simply add.

- It reduces the base upon which future compounding occurs.

This matters more in moderate return environments. In high-return vintages, fee drag may be partially obscured. In lower-return or volatile markets, layering becomes more visible.

Performance Fee Layering

Performance fees introduce another layer of structural compounding.

If an allocator pays:

- A carry or incentive fee at the underlying manager level, and

- A performance-based fee at the fund-of-funds level,

The effective share of upside retained by the allocator may be meaningfully reduced.

This does not imply that performance fees are inappropriate. Incentive alignment can be valuable. But layering alters the distribution of gains.

Importantly, the impact of layered performance fees becomes more pronounced when:

- Gross returns compress

- Volatility increases

- Recovery periods extend

- Under those conditions, net return dispersion widens.

Embedded Cost Opacity

Layered structures can also introduce reporting complexity:

- Underlying expense allocations

- Monitoring fees

- Transaction-level costs

- Financing spreads

These costs may be disclosed, but attribution becomes less intuitive when capital flows through multiple entities.

From a governance standpoint, our view is that fee drag is not only about percentage points — it is about visibility and compounding arithmetic.

Lens #2 — Incentive Alignment: Discretion and Risk Under Stress

Alignment is frequently discussed in general terms. Structurally, it relates to how discretion is exercised and who bears the consequences of that discretion.

Incentives in Layered Structures

In a multi-tiered structure:

- The underlying manager is incentivized based on their fund’s performance.

- The top-level vehicle is incentivized based on aggregate portfolio outcomes.

- The allocator ultimately bears economic exposure.

- These incentives can align. But they are not identical.

- For example:

- An underlying manager may prioritize protecting their fund-level IRR metrics.

- A fund-of-funds manager may prioritize smoothing volatility across managers.

- An allocator may prioritize capital preservation over interim marks.

- These distinctions tend to surface most clearly in downturns.

Discretion in Down Markets

When markets contract, decision pressure increases:

- Extend or enforce?

- Inject rescue capital or preserve dry powder?

- Mark conservatively or defend prior valuations?

In layered structures, discretion is exercised at multiple levels. The allocator’s influence may be advisory rather than directive.

In direct oversight structures, governance authority over these decisions tends to be centralized. That does not eliminate risk. It clarifies who holds responsibility.

The issue is not whether one model performs better in downturns. It is whether incentive misalignment in funds can emerge when objectives diverge under stress.

Alignment as Governance Principle

In our view, alignment should be approached less as a marketing claim and more as an institutional design question:

- Who controls underwriting authority?

- Who controls modifications?

- Who absorbs downside first?

- Who determines exit timing?

- In a well-designed structure, these answers are explicit.

When they are implicit or diffused, allocators rely more heavily on trust and reputation.

Both may be valid approaches. But they differ in governance clarity.

Shoora Capital

Talk to us about which structure fits your portfolio.

Shoora deploys capital with direct oversight into middle market real estate — where governance clarity and operator alignment are built into the structure from day one.

Get in touch →Lens #3 — Control: Underwriting, Decision Rights, and Governance

The most substantive distinction between direct oversight vs fund model often lies in underwriting control.

Underwriting is not merely deal selection. It includes:

- Credit box definition

- Sponsor eligibility criteria

- Leverage thresholds

- Geographic concentration limits

- Duration parameters

- Extension policies

- Workout authority

Where Decision Rights Sit

In a fund-of-funds structure:

- Underwriting authority resides primarily with underlying managers.

The top-level vehicle conducts due diligence but does not typically control asset-level decisions.

Advisory rights may exist but are rarely unilateral.

In a direct oversight structure:

- The governing entity establishes and monitors underwriting parameters.

- Investment committees retain authority over capital deployment.

- Modifications and workouts follow defined policy processes.

- The distinction is one of decision rights, not competence.

Governance of Underwriting

Underwriting governance matters most when assumptions fail.

For example:

- If interest rates rise faster than modeled,

- If liquidity tightens,

- If sponsor equity erodes,

- Who decides whether to extend, restructure, or enforce?

- Clarity of decision authority reduces ambiguity during stress.

Consider a scenario where interest rates rise 250 basis points, exit timelines extend 18 months, and sponsor liquidity deteriorates. In a layered structure, the allocator’s influence over extension decisions may be indirect. In a direct oversight structure, underwriting authority can reassess leverage thresholds, covenant tolerance, and capital reserves within a centralized governance framework.

The discipline required to define those parameters in advance is discussed separately in Shoora’s framework on underwriting governance and execution integrity — see our direct vs. fund comparison. The structural question addressed here is who ultimately holds that rigor accountable.

Transparency in decision authority often correlates with faster response times and fewer internal conflicts during adverse conditions.

A Practical Allocator Framework: Questions to Ask Before Choosing a Structure

Rather than prescribing a preferred model, allocators may benefit from a structured evaluation process.

The following checklist can serve as a reusable allocator decision framework.

1. Where Does Discretion Sit?

Who approves new investments?

Who has authority to override underwriting recommendations?

Who controls capital calls and extensions?

Discretion concentrated in one entity differs from discretion distributed across tiers.

2. How Are Conflicts Resolved?

What formal mechanisms exist for dispute resolution?

Are LP advisory committees advisory or binding?

How are related-party transactions handled?

Conflict resolution protocols are rarely tested in strong markets. They matter in contractions.

3. What Reporting Transparency Exists?

Can capital be traced to the asset level?

Are expense allocations clearly delineated?

Is performance attribution segmented by strategy and decision cohort?

Transparency influences the allocator’s ability to diagnose performance drivers.

4. Who Owns Underwriting Authority?

Is underwriting centralized or delegated?

Are credit parameters documented?

Are deviations from policy recorded?

Ownership of underwriting authority defines accountability.

5. How Is Performance Attribution Tracked?

Are returns segmented by manager, strategy, and vintage?

Can fee impact be isolated?

Is net performance reconciled across tiers?

Layered structures make attribution more complex. That does not make them inappropriate. It makes analysis more necessary.

These questions do not produce a binary answer. They clarify trade-offs.

Structure Selection Framework

Choose direct oversight if…

- Governance clarity and accountability are a priority

- You require visibility into asset-level decisions

- Incentive alignment under stress is a primary concern

- Fee transparency and single-tier cost structure matter

Consider fund model if…

- Diversification across managers or strategies is the goal

- Access to specialized or niche managers is valued

- Manager selection is preferable to direct underwriting oversight

- Portfolio construction across strategies outweighs governance concentration

Why Shoora Chooses Direct Oversight

Shoora’s preference for direct oversight is a governance philosophy rather than a market critique.

The view is structural:

- Control is a form of risk management.

- Alignment contributes to durability.

- Transparency is not optional; it is structural.

In Shoora’s framework, concentrating underwriting authority and decision rights within a defined governance structure reduces ambiguity about responsibility. It does not eliminate risk. It narrows interpretive gaps when risk materializes.

In practice, that means every transaction is unanimously approved by a three-person Investment Committee, underwritten to a minimum 1.25x DSCR, with individual LTV capped at 75%, and personal guarantees plus borrower co-investment required on every deal.

This philosophy is outlined in greater detail within Shoora’s investment approach. The emphasis is on structural clarity rather than structural complexity.

There are environments where diversified fund exposure may be appropriate. There are others where tighter governance may be prioritized.

Shoora’s position is that governance architecture should be explicit, documented, and internally coherent.

From Structure to Documentation: How Governance Becomes Visible

Governance is only meaningful if it is observable.

An investment governance structure must translate into:

- Written credit parameters

- Documented committee approvals

- Recorded dissent or conditional approvals

- Defined authority thresholds

- Transparent modification policies

- Without documentation, governance becomes narrative.

The practical manifestation of governance is the investment committee memorandum.

An IC memo is not marketing material. It is an accountability instrument. It clarifies:

- Assumptions

- Sensitivity analysis

- Risk flags

- Decision rationale

- Conditional approvals

When allocators evaluate managers or structures, reviewing how decisions are documented often reveals more than reviewing return summaries.

For a structural example of how decision-making is documented and made transparent, our capital stack framework.

If you are evaluating managers or structures, examine how governance is documented and how decision rights are defined.

In Shoora’s view, structure determines incentives. Documentation reveals whether those incentives are operationalized.

Frequently Asked Questions

What is the difference between direct oversight and a fund-of-funds structure?

A direct oversight structure is one in which the capital provider retains authority over underwriting standards, capital deployment decisions, and portfolio governance. Investment teams or operating partners may execute transactions, but investment criteria, leverage parameters, and portfolio decisions are established within a centralized governance framework.

In a fund-of-funds structure, capital is allocated to external managers who control underwriting and asset-level decisions. The allocator’s role focuses primarily on manager selection and portfolio allocation, rather than direct investment governance. As a result, underwriting authority and day-to-day decision-making are distributed across multiple underlying managers rather than concentrated in a single governance structure.

Why do fund-of-funds structures often involve layered fees?

Fund-of-funds structures typically introduce multiple fee layers because capital passes through more than one investment vehicle before reaching the underlying assets. In many structures, investors may encounter management fees at the fund-of-funds level, management fees charged by underlying managers, and performance or incentive fees at one or both layers. Each individual fee may appear reasonable on its own. However, when multiple layers apply simultaneously, they can reduce the portion of gross returns ultimately retained by the allocator.

How does governance differ between direct investment oversight and delegated fund management?

Governance differs primarily in where decision authority resides. In a direct oversight structure, underwriting standards, leverage limits, and portfolio decisions are typically established within a centralized governance framework. Investment committees or internal policy structures retain authority over capital deployment, extensions, and restructuring decisions.

In a delegated fund structure, governance is distributed across several entities. Underwriting and asset-level decisions are generally made by the underlying managers, while the allocator exercises oversight indirectly through due diligence processes, reporting requirements, and advisory committee participation. The allocator’s influence therefore tends to be advisory rather than directive.

When might a fund-of-funds structure be appropriate for investors?

A fund-of-funds structure may be appropriate when investors prioritize diversification, specialized expertise, or access to managers that would otherwise be difficult to reach directly. Allocators seeking exposure across multiple strategies, geographies, or niche asset classes may use a fund-of-funds approach to build diversified portfolios through established managers. In these cases, the value proposition centers on manager selection and portfolio construction, rather than direct underwriting control. The appropriate structure ultimately depends on the allocator’s objectives, governance preferences, and tolerance for delegated investment authority versus centralized oversight.