Key Takeaways

- Rental properties and real estate funds are backed by the same underlying assets but deliver fundamentally different investor experiences — control, liquidity, and risk diverge at the structural level, not at the margins.

- Reported volatility in private real estate is systematically understated due to appraisal smoothing; economic risk accumulates beneath the surface even when appraised values appear stable.

- Rental property concentrates decision-making and risk at the asset level — rewarding operational skill but exposing owners to tenant concentration, local economic shocks, and unpredictable capital costs.

- Real estate funds trade control for diversification and professional management, but impose fee drag and liquidity conditions that may tighten precisely when capital is most needed.

- Choosing the right structure is less about maximizing headline returns and more about matching the investment’s demands — time, operational involvement, liquidity needs — to the investor’s actual constraints.

I. Introduction: Two Ways to Own the Same Asset Class — With Very Different Trade-Offs

At first glance, the choice between owning a rental property and investing through a real estate fund appears straightforward — after all, real estate is real estate. In both cases, the investor is ultimately seeking exposure to income-producing property: rents paid by tenants, property values supported by local economic conditions, and long-term appreciation tied to inflation and growth. This surface similarity has led many investors to treat direct ownership and fund-based real estate as interchangeable routes to the same destination.

That equivalence, however, is largely false.

While rental properties and real estate funds are backed by the same underlying assets — commercial buildings, apartments, or single-family homes — the structure through which ownership is held fundamentally reshapes the investment experience. Control, liquidity, and risk characteristics differ not at the margins, but at the intrinsic nature of the two investment vehicles. Two investors may earn similar long-run average returns from “real estate,” yet arrive there through radically different paths, with very different demands on capital, time, and temperament.

Academic research helps explain why. Studies comparing public and private real estate show that long-run return characteristics can converge, particularly when examined over full market cycles. Hoesli & Oikarinen (2021), for example, find that listed real estate (such as Real Estate Investment Trusts, or REITs) and direct real estate exhibit broadly similar long-term behavior once short-term market noise is stripped away. This has often been interpreted — incorrectly — as evidence that the choice between owning a rental and owning a fund is largely cosmetic.

But other work makes clear why investors’ lived experience can diverge dramatically. Geltner, MacGregor, and Schwann demonstrate that private real estate, whether held directly or through private funds, often appears less volatile primarily because it is valued using appraisals that adjust slowly — a phenomenon known as appraisal smoothing, where infrequent valuations mask real-time changes in economic conditions. Public real estate, by contrast, is continuously priced in liquid markets, producing higher reported volatility even when underlying property cash flows change only modestly. In other words, differences in valuation methodology can mask or exaggerate risk, depending on the structure chosen.

Beyond volatility, structure governs nearly everything else that matters to investors. A rental property offers granular control over leverage, tenants, and capital expenditures, but demands time, operational skill, and tolerance for idiosyncratic risk. Real estate funds offer diversification and professional management, but impose fees, limit control, and often constrain liquidity precisely when it is most valuable. Taxes, too, follow structure, influencing not just how much return is earned, but when and in what form it is realized.

This article examines these trade-offs directly. Rather than asking which option produces the highest headline return, it asks a more practical question: given your constraints, objectives, and willingness to be involved, which structure delivers the best net outcome?

Shoora Capital

Shoora Ground Level

Institutional-grade analysis on Sun Belt real estate, delivered directly to family offices and sophisticated investors. No noise. No marketing. Just the signals that matter — before they show up in the data.

Sign up for Ground Level →II. Return Generation: How the Money Is Actually Made

Understanding the difference between rental property investing and real estate funds begins with a clear view of how returns are generated in practice — not how they are marketed. Although both ultimately rely on rent paid by tenants and the value of underlying property, the path from tenant rent to investor return differs materially depending on whether ownership is held at the property level or the portfolio level.

A. Rental Property: Property-Level Cash Flow and Equity Growth

In essence, a rental property is a small operating business tied to a single asset (or a small cluster of assets). The mechanics of return generation are relatively transparent:

Gross rent → operating expenses → net operating income (NOI) → debt service → free cash flow

Gross rent reflects local market conditions and tenant quality. From this, the owner subtracts operating expenses, property taxes, insurance, repairs, management fees (if any), utilities, and reserves. The resulting NOI — net operating income — is the fundamental economic engine of the property. After servicing mortgage debt, what remains is free cash flow to the owner.

Beyond cash flow, rental properties generate returns through equity growth, driven by three primary mechanisms. First, rent growth increases NOI over time, directly supporting higher property values. Second, capitalization rate (cap rate) movements — where a cap rate is the ratio of NOI to property value, and the key metric investors use to price income-producing real estate — whether from falling interest rates, improving neighborhood desirability, or tighter investor demand, can reprice the same income stream at a higher valuation multiple. Third, and uniquely for direct owners, forced value creation through capital expenditures and active management can increase NOI independently of broader market conditions. Renovations, re-tenanting, operational efficiencies, or rezoning can all raise value in ways that are not purely passive.

These mechanics mean that returns from rental properties are heavily shaped by owner-specific decisions. Local rent dynamics matter enormously; a well-located property in a growing labor market can experience materially different outcomes from an otherwise similar property in a stagnant area. Financing terms — loan-to-value ratios, interest rates, amortization schedules, and refinancing decisions — directly affect both cash flow and equity accumulation. This mechanism cuts both ways: the same leverage that amplifies gains during appreciation periods magnifies losses when values decline or refinancing conditions tighten. Timing also plays a critical role: the price paid at acquisition and the conditions prevailing at exit can dominate multi-year holding period returns.

However, this property-level focus introduces distinct risks. Tenant concentration is unavoidable: one vacant unit in a single-family rental represents a 100% loss of rental income until re-leased. Local economic shocks — such as the closure of a major employer or changes in zoning or taxation — disproportionately affect individual properties. Capital expenditure surprises — roof replacements, structural repairs, or regulatory compliance upgrades — can erase years of expected cash flow. These risks are not diversified away; they are borne entirely by the owner.

It is worth noting that rental property dynamics vary meaningfully by sub-type. Single-family residential, small multifamily, and commercial properties each carry different concentration profiles, management demands, and financing structures. The dynamics described here are most characteristic of residential and small multifamily ownership; commercial rental properties introduce additional lease complexity and tenant credit considerations.

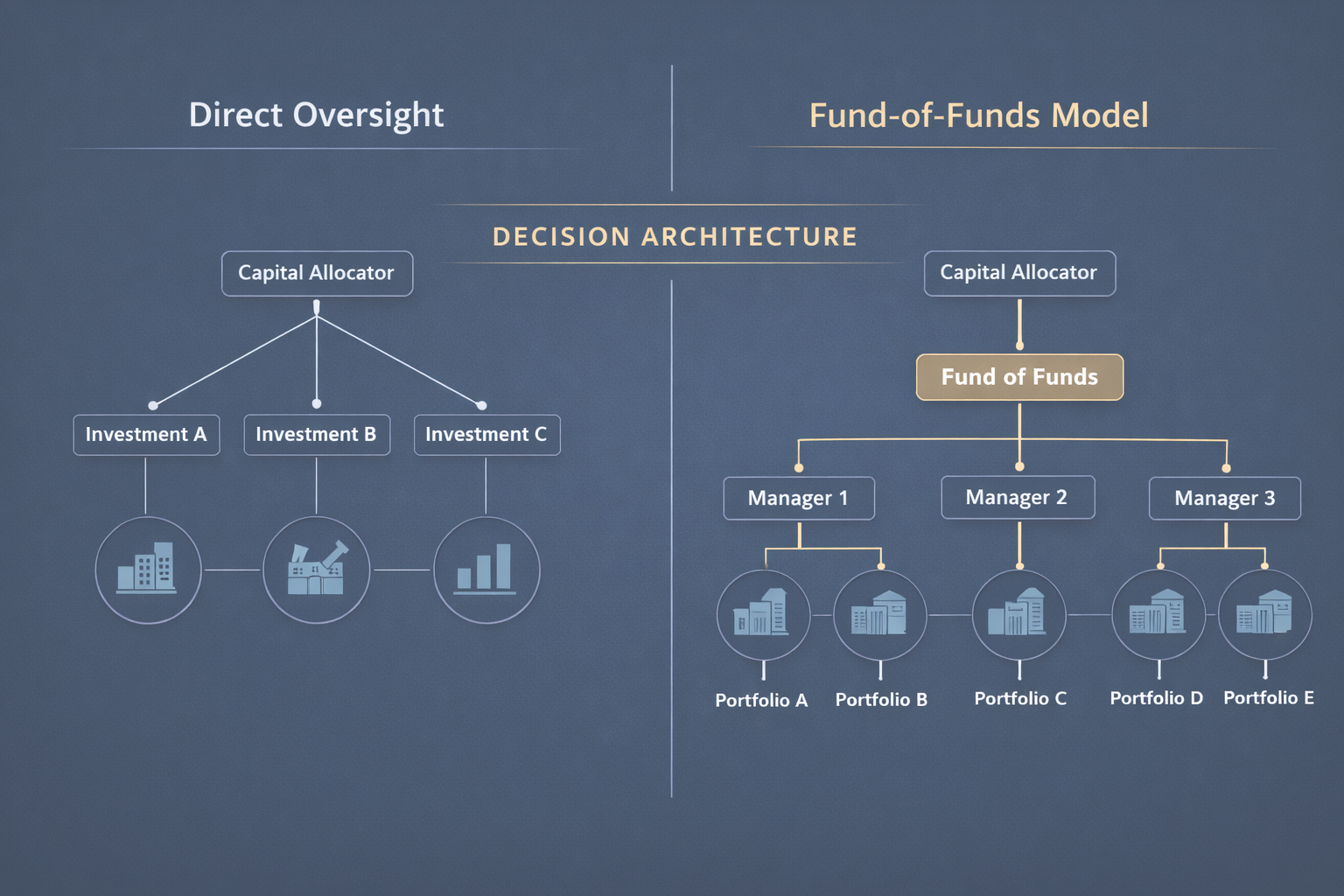

B. Real Estate Funds: Portfolio-Level Exposure

Real estate funds operate at a fundamentally different level of aggregation. Instead of owning one or a handful of properties, investors gain exposure to a portfolio of assets, with returns generated from pooled NOI, changes in asset valuations, and leverage policies established by the fund manager. This structure can take several forms, ranging from publicly listed Real Estate Investment Trusts (REITs) — companies that own income-producing properties and trade on public exchanges like stocks — to private core funds such as Open-End Diversified Core Equity (ODCE)-style vehicles, and extending to value-add or opportunistic private equity strategies.

In all cases, the mechanics are similar in principle but different in execution. Rental income from dozens or hundreds of properties is aggregated at the portfolio level. Operating costs and debt service are managed centrally. Investors receive returns net of fund expenses, with distributions and net asset value reflecting the combined performance of the underlying assets. Unlike direct ownership, individual asset-level decisions are typically opaque to the end investor.

Return drivers in this context shift from micro-level execution to portfolio construction and policy choices. Asset selection and sector weighting — such as the proportion allocated to apartments versus industrial or office properties — strongly influence performance. Leverage decisions, often applied both at the property and entity level, can amplify returns but also increase downside risk. Crucially, fee drag becomes a structural component of returns: management fees, operating expenses, and in some cases performance fees reduce gross property returns before they reach investors.

Academic and institutional research helps clarify how these differences play out empirically. Cotter & Roll (2011) show that REIT returns often diverge from residential real estate price indexes in the short run, reflecting differences in leverage, sector composition, and public market pricing — even though both are ultimately linked to property fundamentals. This helps explain why fund-based real estate may feel more “equity-like” at times, despite owning tangible assets.

Similarly, institutional analyses such as the Teachers Insurance and Annuity Association (TIAA) private real estate research highlight that differences in reported performance between listed and private real estate are often driven less by underlying income generation than by valuation methodology, leverage, and fees. Portfolio diversification dampens idiosyncratic property-level risk, but it also removes the ability for individual investors to add value through hands-on management.

Comparing the Two Paths

The contrast between rental properties and real estate funds is therefore not a question of what generates returns — both rely on rents and property values — but of where decisions are made and who bears specific risks. Rental properties concentrate return generation and risk at the asset level, rewarding skill, timing, and operational involvement while exposing the owner to idiosyncratic shocks. Real estate funds abstract those same cash flows into portfolio-level exposure, trading control and transparency for diversification, scale, and professional management.

As subsequent sections will show, these structural differences cascade into divergent experiences of volatility and liquidity. What appears, at first glance, to be the same asset class is in practice two very different ways of turning property income into investor returns.

III. Risk, Volatility, and the Illusion of Stability

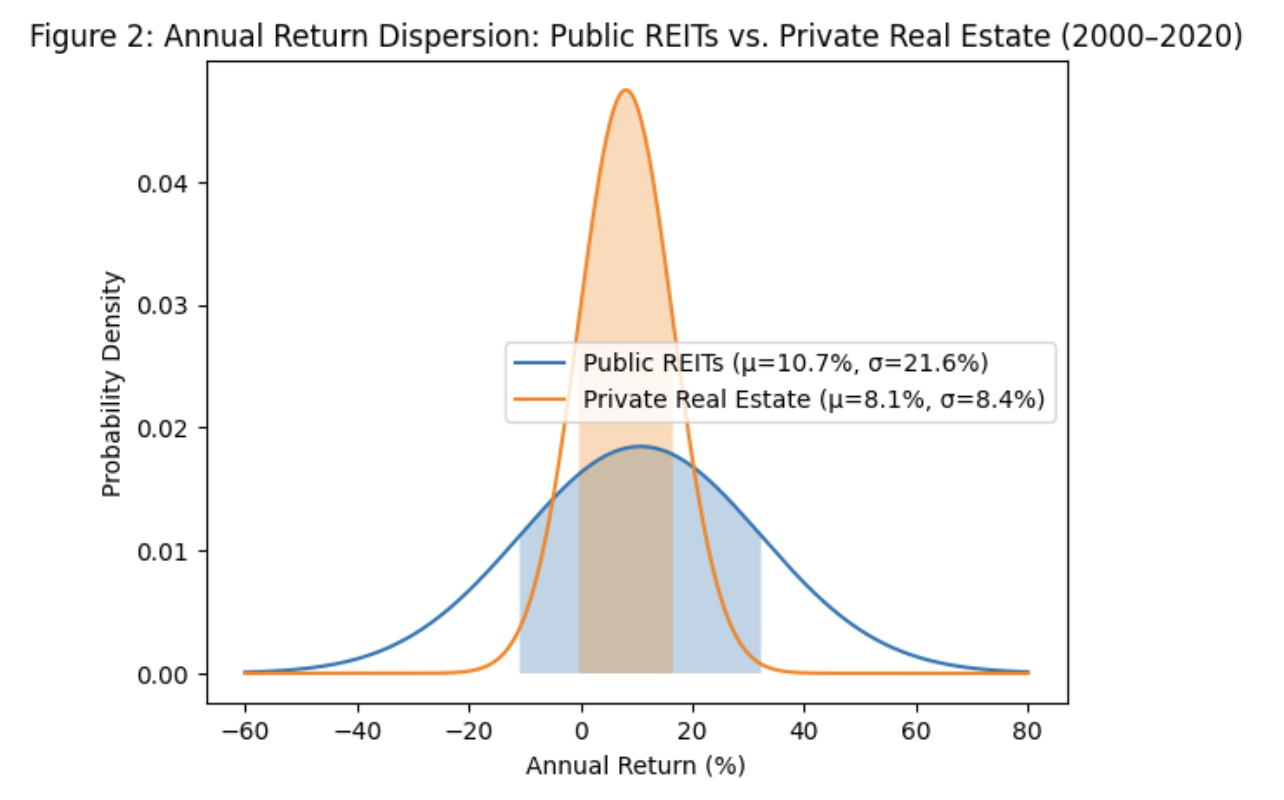

Risk is often the most misunderstood dimension in the rental property versus real estate fund debate. Investors frequently rely on reported volatility — standard deviation of returns, drawdowns, or price fluctuations — to assess relative safety. Yet academic research shows that reported volatility in real estate frequently reflects how assets are priced, not just the underlying economic risk they carry. As a result, rental properties and private real estate funds can appear deceptively stable when compared to publicly traded real estate, even though their fundamental exposures may be similar.

A. Reported Volatility vs. Economic Risk

Private real estate, whether owned directly as a rental or indirectly through a private fund, is typically valued using appraisal-based methodologies. Appraisals rely on comparable transactions, income capitalization models, and professional judgment — all of which update infrequently and incorporate a degree of smoothing. Because appraisals lag real-time market conditions, measured returns tend to adjust slowly, producing lower reported volatility.

Geltner, MacGregor, and Schwann demonstrate that this appraisal smoothing effect leads to a systematic understatement of true economic volatility in private real estate indexes. The absence of frequent trading does not mean that property values are stable; it means that changes in value are not immediately observed. When market conditions deteriorate — rising interest rates, falling rents, tightening credit — private real estate values do not instantly reprice, but economic risk nonetheless accumulates beneath the surface.

Publicly traded REITs, by contrast, are continuously priced in liquid capital markets. Their share prices incorporate not only current property cash flows, but also investors’ expectations about future rents, financing conditions, and macroeconomic risk. This produces higher short-term volatility and sharper drawdowns, particularly during periods of financial stress. Importantly, however, higher reported volatility does not necessarily imply higher underlying property risk. In many cases, REIT prices adjust faster to information that private market valuations will only reflect months or years later.

Hoesli & Oikarinen (2021) reinforce this distinction by showing that, over longer horizons, the return characteristics of listed and direct real estate tend to converge. Short-run volatility differences largely dissipate when examined across full market cycles, suggesting that the apparent stability of private real estate is, to a significant degree, an artifact of valuation methodology rather than superior risk control.

For individual investors, this has practical implications. A rental property that appears “low volatility” because its appraised value changes little from year to year may still be highly exposed to interest rate shocks, local employment trends, or refinancing risk. Conversely, a REIT investment that fluctuates daily may be providing a more transparent — if emotionally challenging — signal of changing economic conditions.

B. Concentration Risk

Beyond valuation effects, concentration risk is often a more consequential driver of outcomes than volatility statistics. A single rental property represents exposure to one asset, one geographic market, and often one tenant base. A vacancy, major repair, or neighborhood decline can have an outsized impact on cash flow and value. Even small portfolios of rentals remain vulnerable to correlated local shocks.

Real estate funds mitigate this risk through diversification across properties, regions, and tenants. Portfolio-level exposure reduces the impact of any single asset’s underperformance. That said, diversification is not absolute. Funds may still concentrate by sector — such as apartments, office, or industrial — or by strategy, such as value-add or opportunistic investing. Sector-wide downturns can therefore affect fund performance materially, even when individual asset risk is diversified away.

Takeaway

The key lesson is that volatility metrics alone are misleading when comparing rental properties and real estate funds. Appraisal-based smoothing can mask economic risk, while market pricing can exaggerate short-term fluctuations. In practice, concentration and leverage often matter more than reported volatility. Investors who focus solely on smooth returns may underestimate risk, while those who fixate on price swings may overestimate it. Understanding how risk is structured — and how it is revealed over time — is essential to making an informed choice between direct and fund-based real estate ownership.

IV. Liquidity: When Can You Actually Access Your Capital?

Liquidity — how quickly and reliably an investor can convert an asset into cash — is one of the most practical yet underappreciated dimensions separating rental properties from real estate funds. While both offer exposure to income-producing property, they sit at opposite ends of the liquidity spectrum, and the difference becomes most consequential precisely when market conditions deteriorate or capital is urgently needed.

A. Rental Property Liquidity

Rental property is inherently illiquid. Exiting an investment typically involves a multi-step process: marketing the property, negotiating price and terms, completing inspections, securing buyer financing, and closing the transaction. Even in favorable markets, this process can take months, and in weaker conditions it can stretch significantly longer.

Transaction costs further erode effective liquidity. Brokerage commissions, legal fees, transfer taxes, and potential price concessions routinely absorb several percentage points of gross sale value. Unlike liquid securities, where bid–ask spreads are measured in basis points, property transactions impose large, discrete costs that discourage frequent rebalancing or partial exits.

Perhaps more importantly, there is price uncertainty until the sale closes. Appraised values or online estimates provide only rough guidance; the true market price is revealed only when a willing buyer commits capital. In periods of rising interest rates or tightening credit, buyers may re-trade or fail to close, introducing execution risk even after a nominal price has been agreed. For investors relying on property sales to meet liquidity needs — such as funding retirement expenses or reallocating capital — this uncertainty can be material.

The illiquidity of rental property is not necessarily a flaw; for some investors, it imposes discipline and reduces the temptation to trade emotionally. But it does mean that capital is effectively locked in, with limited flexibility to respond quickly to changing circumstances.

B. Fund Liquidity

Real estate funds offer a wide range of liquidity profiles, depending on structure.

Publicly listed REITs provide the highest degree of liquidity. Shares can be bought or sold daily at transparent market prices, allowing investors to rebalance portfolios or raise cash almost instantly. However, this liquidity comes with a trade-off: REIT prices are influenced not only by underlying property cash flows, but also by broader equity-market sentiment, interest rate expectations, and risk appetite. During market stress, REIT prices may fall sharply, even if property-level fundamentals adjust more slowly.

Academic work on REIT liquidity — including research from Hoesli & Oikarinen (2021) — highlights that this distinction is one of timing rather than substance. REIT markets often incorporate information about deteriorating property conditions well before those changes appear in private-market transactions or appraisals. Daily liquidity does not eliminate exposure to real estate cycles; it simply reveals them more rapidly.

Private real estate funds occupy a middle ground. Many offer periodic redemption windows — quarterly or annually — but with important caveats. Redemption requests may be subject to gates, limiting the percentage of fund assets that can be withdrawn at any one time. In stressed markets, funds may impose queues or temporary suspensions to protect remaining investors and avoid forced asset sales. Research from the European Association for Investors in Non-Listed Real Estate Vehicles (INREV) on illiquidity premiums and benchmarking studies from CEM Benchmarking — an independent institutional investment data firm — and Nareit (National Association of Real Estate Investment Trusts) shows that private fund liquidity terms are not theoretical features; they are structural constraints that have been exercised during prior market dislocations, precisely when investors most desired access to capital.

Liquidity as a Strategic Constraint

The critical insight is that liquidity should not be evaluated in isolation, but in relation to when liquidity is needed. Rental properties provide control but little flexibility. REITs provide flexibility but expose investors to market repricing. Private funds promise liquidity, but only conditionally.

From an institutional perspective, investors are compensated for bearing illiquidity risk over long horizons — but only if they can tolerate the constraints when markets seize up. For individual investors, the choice between rentals and funds is therefore less about which asset is “more liquid” in theory, and more about which liquidity profile aligns with their cash flow needs, risk tolerance, and time horizon.

In real estate, the question is not whether liquidity matters, but when you will need it — and under what conditions you can actually get it.

V. Conclusion: Choosing the Structure That Fits the Investor, Not the Asset

The comparison between rental properties and real estate funds ultimately reveals a central insight: the asset class is the same, but the investor experience is not. Both approaches are rooted in income-producing property, both derive value from rents and long-term appreciation, and — over sufficiently long horizons — academic evidence suggests their aggregate return characteristics may converge. Yet, as the preceding sections have shown, how those returns are generated, how risks are revealed, and how capital can be accessed differ in ways that materially shape outcomes for real-world investors.

Rental property ownership concentrates decision-making and risk at the asset level. Returns are driven by local rent dynamics, financing choices, and the owner’s ability to manage operations and capital expenditures. This structure rewards skill, patience, and active involvement, but it also exposes the investor to tenant concentration, local economic shocks, and unpredictable capital costs. Liquidity is limited, exit pricing is uncertain, and capital is effectively committed until a sale can be executed — often at significant cost. For investors willing to treat real estate as an operating business, these constraints can be acceptable, even advantageous, but they are real and unavoidable.

Real estate funds, by contrast, abstract property ownership into portfolio-level exposure. Diversification across assets, tenants, and regions reduces idiosyncratic risk, and professional management shifts day-to-day execution away from the investor. Liquidity improves — dramatically so in the case of listed REITs — but at the price of market repricing and, in private funds, conditional redemption terms that may tighten precisely during periods of stress. Fees and leverage policies become structural features of returns, and individual investors relinquish control over asset selection, timing, and capital allocation.

Perhaps most importantly, reported volatility and headline returns can be misleading guides. Appraisal-based valuations smooth private real estate returns, masking underlying economic risk, while public markets reveal that risk more quickly and visibly. Concentration, leverage, liquidity constraints, and workload often matter more than standard deviation figures when determining whether an investment succeeds or fails for a particular investor.

The practical conclusion is not that one approach is inherently superior. The better choice depends on constraints: time availability, tolerance for operational involvement, liquidity needs, tax circumstances, and behavioral preferences. Investors who optimize solely for gross returns risk overlooking the frictions that determine net outcomes. And no framework — however thorough — can eliminate the execution risk, market timing, and unforeseen conditions that shape real outcomes over a full cycle.

In real estate, structure is not a technical detail — it is the investment. Choosing between rental properties and real estate funds is less about selecting an asset class and more about selecting the set of trade-offs you are prepared to live with through market cycles, execution challenges, and conditions that cannot be fully anticipated in advance.

Frequently Asked Questions

Which produces better returns — rental property or real estate funds?

Neither is categorically superior. Academic research shows that over long horizons, return characteristics can converge. What diverges is how those returns are generated and what the investor must contribute to earn them. Rental properties can generate strong returns for investors who are actively involved and skilled at the asset level. Funds deliver returns net of fees and through diversified exposure, with professional management doing the operational work. The more useful question is not which returns are higher in gross terms, but which structure delivers better net outcomes given your fees, taxes, time costs, and execution capability.

Is rental property really that illiquid? Can’t I just sell it?

Yes — but on the market’s timeline, not yours. Even in strong conditions, a property sale typically takes 60–120 days from listing to close, with transaction costs of 6–8% of gross value absorbing brokerage, legal, and transfer expenses. In weaker markets, buyer financing can fall through after agreement, extending timelines further. Capital is effectively committed until those steps complete. Private real estate funds offer periodic redemption windows, but those windows can be gated or suspended during stress — precisely when liquidity is most needed. Listed REITs are the only structure that provides genuine daily liquidity, though at the cost of daily market repricing.

If private real estate looks stable, doesn’t that mean it’s lower risk?

Not necessarily. The apparent stability of private real estate valuations — including direct rental property — reflects how infrequently those assets are appraised, not the underlying economic risk they carry. Academic research by Geltner, MacGregor, and Schwann demonstrates that appraisal-based returns systematically understate true economic volatility. Risk accumulates beneath the surface during deteriorating conditions even when appraised values hold steady. Investors who equate smooth reported returns with low risk may be underestimating their actual exposure to interest rate shocks, refinancing risk, and local market deterioration.

What happens to fund liquidity when markets turn?

This is where liquidity promises are tested. Private real estate funds commonly include gates — provisions that allow the fund to limit redemptions to a percentage of fund assets per period — and suspension rights that can pause withdrawals entirely. These are not hypothetical features. They have been exercised during prior downturns precisely because funds must avoid forced asset sales that would harm remaining investors. Institutional benchmarking data documents this pattern. If you are investing in a private fund, read the redemption terms carefully and assume that liquidity will be most restricted when you most want it.

How do fees affect my actual return in a real estate fund?

Materially. Fund fees typically include a management fee (commonly 1–2% of assets annually), plus, in many cases, acquisition and disposition fees, and a performance fee or carried interest (often 20% of profits above a preferred return threshold). These fees compound over time and can meaningfully widen the gap between gross property returns and what the investor actually receives. Always evaluate fund performance on a net-of-fee basis, and understand the full fee waterfall before committing capital. Headline returns without fee context are not a reliable guide to net investor outcomes.

Disclaimer: This content is for educational and informational purposes only and should not be construed as investment advice. Real estate investments involve risk, including potential loss of principal. Past performance does not guarantee future results. Consult with qualified financial, legal, and tax professionals before making investment decisions.