Key Takeaways

- Private real estate investments have historically delivered competitive long-term returns with lower reported volatility than public REITs over certain multi-decade periods, e.g., 2000–2020.

- It has demonstrated low correlation to public equities and bonds, improving portfolio diversification.

- Income returns have historically represented a significant portion of total return, supporting cash-flow stability.

- Institutional investors commonly maintain 10–15% strategic allocations to real estate.

- Access to private markets remains essential for meaningful exposure, as the majority of commercial real estate is privately owned.

When building enduring, multigenerational wealth, sophisticated investors and family offices increasingly ask: why invest in private real estate? The answer lies in a compelling risk-return profile and powerful diversification benefits. Indeed, over certain time frames, private real estate has delivered equity-like returns but with far less volatility, according to the National Council of Real Estate Investment Fiduciaries (NCREIF).

In this article, we will examine the fundamental case for private real estate as a vehicle for long-term capital preservation and growth. We will also explore why many large institutions and family offices maintain a 10–20% allocation to private real estate across economic cycles.

By the end, you’ll understand why private real estate remains a cornerstone for those seeking wealth that endures, across generations.

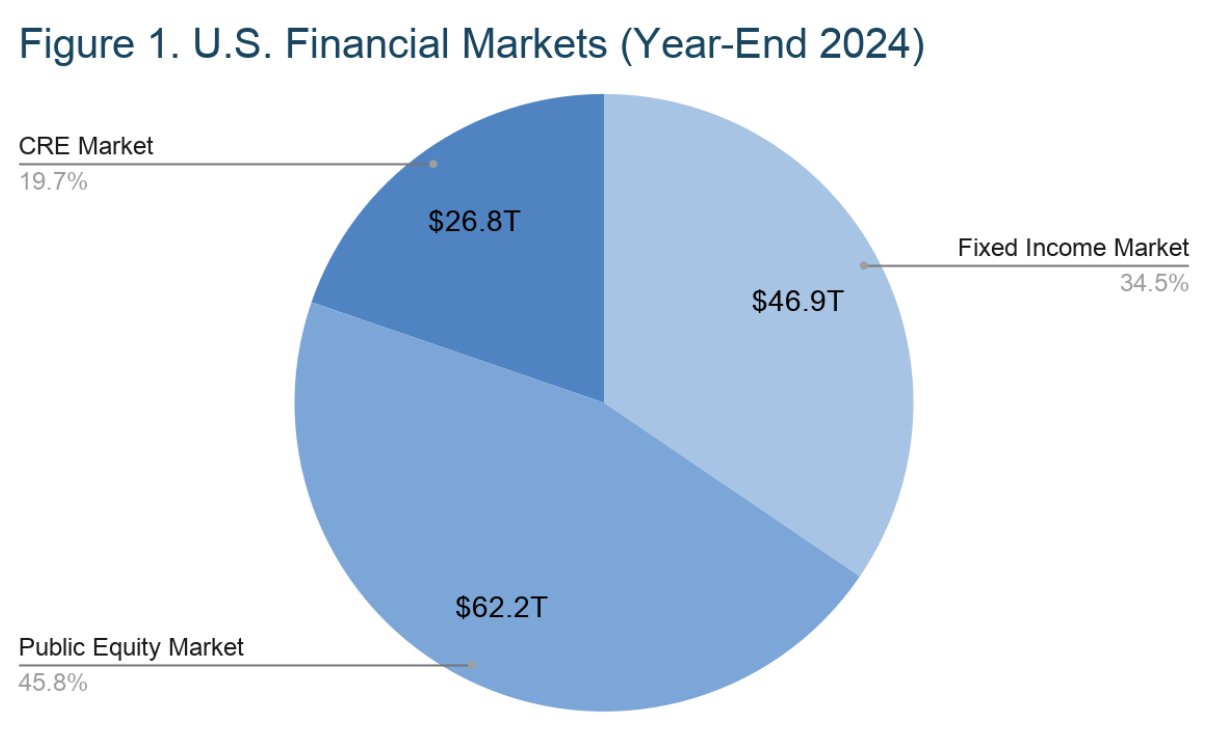

Real Estate: The Third-Largest Asset Class

Real estate, particularly commercial real estate, occupies a place among the giants of investable asset classes, offering investors a compelling hybrid of income and long-term capital appreciation. Private real estate generates steady rental income, while properties often appreciate over time, combining the cash-flow benefits of fixed income with the growth potential of equities.

To appreciate its scale: at year-end 2024, the U.S. fixed income market totaled approximately $46.9 trillion in outstanding securities (SIFMA). By comparison, the estimated value of the U.S. commercial real estate (CRE) market — across office, industrial, retail, multifamily, hospitality, and other property types — was roughly $26.8 trillion (The Real Estate Roundtable, 2024). Meanwhile, the U.S. public equity market stood at approximately $62.2 trillion in total market capitalization at year-end 2024 (Siblis Research).

Data Sources: SIFMA; Real Estate Roundtable; Siblis Research

These figures show that commercial real estate represents a massive, systemic asset class, not a niche “alternative,” but a core component of the investable universe alongside bonds and stocks. That scale underscores real estate’s fundamental economic role: it is indispensable infrastructure for business, housing, commerce, and more, supporting the flow of goods and services, employment, and long-term growth.

For sophisticated investors and family offices seeking lasting wealth, real estate offers a large, liquid (on a market-wide basis), and economically grounded allocation option, capable of delivering both stable cash flow and long-term capital appreciation.

Private Markets: The Primary Way to Invest

For investors seeking meaningful exposure to real estate, private markets, not public NAREIT-listed REITs, remain the dominant arena. Indeed, with 89% of U.S. commercial real estate privately owned (Q4, 2024), private real estate defines the core investable universe.

A commonly cited rule of thumb is an 85/15 split: roughly 85% of commercial real estate sits in private hands, while only about 15% is represented by public REITs. This estimate is supported by NAREIT research.

This split matters a great deal. On one hand, it underscores the reach and depth of opportunity available, far beyond what public markets can touch. On the other hand, it presents a challenge: without access to private funds or direct deals, even large investors may be locked out of much of the real estate opportunity set.

Private markets offer a far broader universe of property types (office, industrial, hospitality, multifamily, niche assets), geographies (core, secondary, tertiary markets), and strategies (core income, value-add, opportunistic, development) than public REITs typically provide. For family offices and long-term investors, accessing private markets is thus essential for building a comprehensive, diversified real estate allocation, one capable of capturing both income and appreciation across economic cycles.

In short: public REITs are only the “tip of the iceberg.” To secure meaningful exposure, and harness real estate’s full risk-return potential, participating in the private markets is more than a preference; it’s a necessity.

Individual Investors Are Significantly Under-allocated

Despite real estate’s scale and its role as a major institutional asset class, individual investors remain markedly under-allocated. Major institutions such as public pensions and university endowments typically commit about 10-15% of their portfolios to real estate and real-asset strategies, reflecting a long-standing recognition of the asset class’s income stability, inflation protection, and diversification value.

Family offices show a similar posture: recent studies place their real-estate allocation at around 11%, with 2025 surveys from Goldman Sachs, indicating a rebound in allocations as families re-engage private markets following recent volatility.

Individual investors, by contrast, remain dramatically behind. Industry research shows that most allocate under 5% to alternatives overall, which includes private real estate, private equity, private credit, and hedge funds combined. This gap is not the result of weaker demand, but of historical access constraints, minimum investment thresholds, accreditation rules, limited product availability, and operational complexity that once made private real estate difficult for individuals to enter.

The barriers traditionally faced by the individual investor are now rapidly falling. Modern private-market vehicles offer lower minimums, simplified structures, improved transparency, and institutional-grade management. As a result, individual investors are beginning to close the gap. The appetite for alternatives, including real estate, is growing, as a recent survey from Blackrock indicates. Seventy-two (72%) of respondents are prepared to invest in private markets.

However, the allocation discrepancy remains large, highlighting a significant opportunity for those seeking to build resilient, multi-generational portfolios grounded in the same principles that guide leading institutions.

Attractive Risk-Adjusted Returns

Private real estate has historically delivered a compelling blend of strong returns and lower volatility, depending on the benchmark and measurement period. This has produced some of the most attractive risk-adjusted outcomes among major asset classes.

Over the 20-year period ending December 31, 2020, the NFI-ODCE Index, the industry’s flagship benchmark for core private real estate, has generated 8.1% annualized returns. This places it within striking distance of the S&P 500’s roughly 12% annualized total return, based on Slickcharts data.

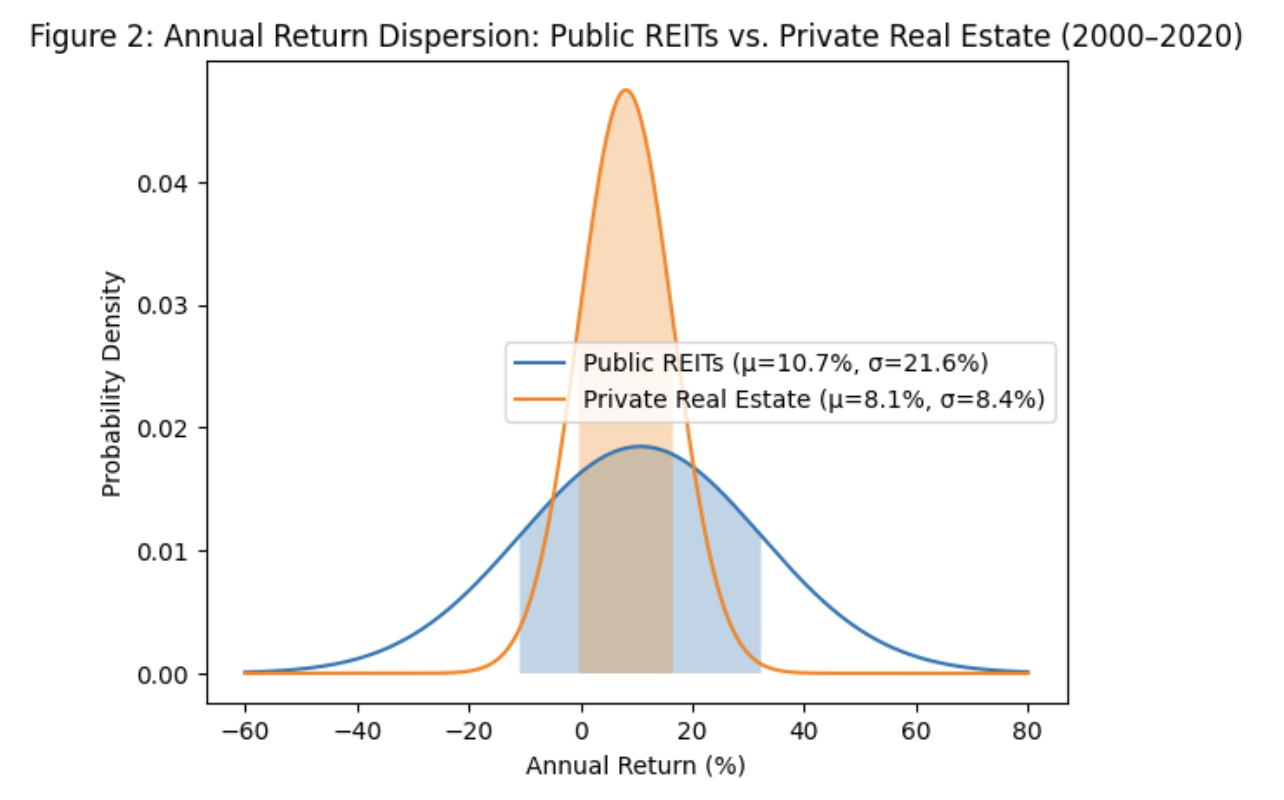

Where private real estate truly differentiates itself is volatility. “Private real estate volatility has been significantly lower than listed REITs and other stock categories, producing a record of higher risk-adjusted returns,” states a TIAA report. By virtue of their public market inclusion, listed REITs are affected by overall market volatility.

Data Source: TIAA

The chart compares the dispersion of annual returns for Public REITs and Private Real Estate from 2000–2020 by plotting normal distributions using their historical mean returns and standard deviations, as supplied by this TIAA Report. Although average returns were close (10.7% for REITs versus 8.1% for private real estate), the width of the distributions differs materially.

Public REITs exhibit a much wider spread (σ = 21.6%), indicating significantly greater year-to-year volatility, while private real estate shows a tighter clustering of outcomes (σ = 8.4%). The shaded ±1σ regions illustrate the range within which approximately 68% of annual returns would be expected to fall, highlighting that REIT returns fluctuated over a range roughly 2.6 times wider than private real estate over the period.

The report compared the NCREIF Fund Index–Open End Diversified Core Equity (NFI–ODCE) for private real estate and FTSE NAREIT U.S. Real Estate Index for listed REITs.

The resulting Sharpe ratios, a measure of risk-adjusted performance, for the twenty-year period January 1, 2000 to December 31, 2020 illustrate the differences: 0.43 for public REITs; 0.78 for private real estate.

Thus, while public REITs did produce higher returns (10.7%) than private real estate (8.1%) over the sample period (January 1, 2000-December 31, 2020), the return patterns differed meaningfully due to structural characteristics of each vehicle.

However, note that public REITs are exchange-listed securities and therefore trade continuously. Their prices adjust in real time to changes in interest rates, equity risk premiums, investor sentiment, and broader macroeconomic conditions. As a result, listed REIT volatility often resembles that of small- and mid-cap equities, reflecting daily liquidity and mark-to-market pricing rather than solely underlying property-level cash flows.

Private real estate, by contrast, reflects the performance of directly held properties. Valuations are typically based on periodic third-party appraisals and transaction comparables rather than continuous market trading. Returns are therefore driven primarily by net operating income, rent growth, occupancy trends, financing structure, and property-level appreciation. This appraisal-based framework produces smoother reported volatility, though it may also delay the recognition of rapid market repricing.

The observed difference in volatility between public REITs and private real estate over the sample period reflects these structural distinctions: one is a liquid, publicly traded equity vehicle; the other is an appraisal-based ownership structure tied more directly to property cash flows. Each serves a distinct role within a portfolio depending on an investor’s objectives for liquidity, transparency, income stability, and sensitivity to public-market movements.

Importantly, outcomes can vary meaningfully across time horizons and market regimes. The comparison between public REITs and private real estate highlights differences in structure and pricing behavior rather than an inherent advantage of one format over the other.

Regardless, private real estate’s blend of competitive returns, moderate volatility, and strong Sharpe ratios makes it a compelling choice for investors focused on durable, risk-adjusted wealth creation.

Shoora Capital

Shoora Ground Level

Institutional-grade analysis on Sun Belt real estate, delivered directly to family offices and sophisticated investors. No noise. No marketing. Just the signals that matter — before they show up in the data.

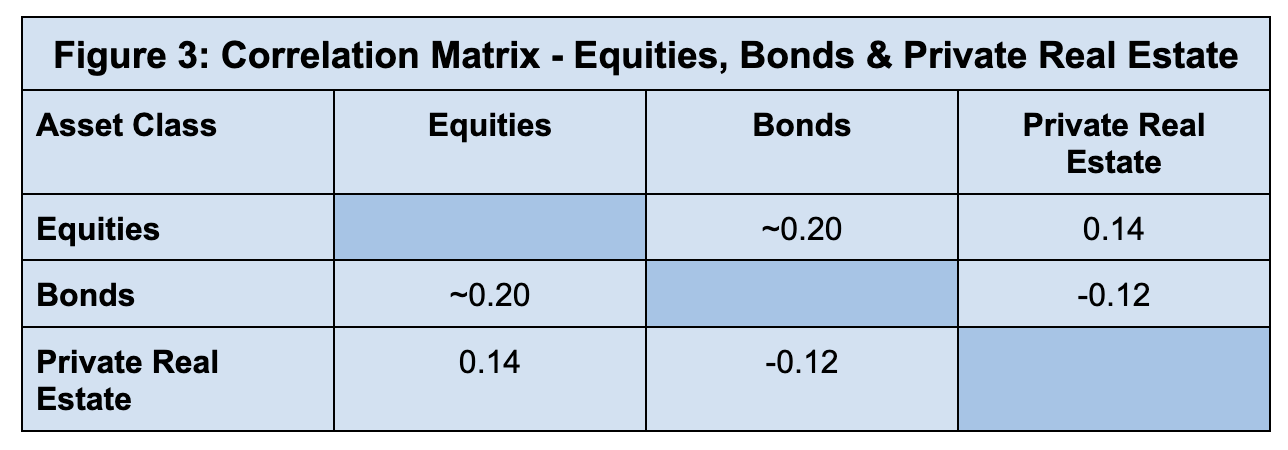

Sign up for Ground Level →Low Correlation: Meaningful Portfolio Diversification

One of private real estate’s most powerful advantages is its consistently low correlation to traditional asset classes. Over the 20 years ending December 2020, the NFI-ODCE Index showed a correlation of just 0.14 with the S&P 500, meaning private real estate often moves independently of, or even counter to, public equities. Correlations with fixed income are even better (-0.12). A portfolio mix of bonds and private real estate is a well-diversified portfolio.

Data Source: TIAA whitepaper, Private Real Estate

To put these numbers in context, correlation coefficients range from –1.0 (assets move in opposite directions) to +1.0 (assets move together perfectly). A correlation below 0.70 is widely accepted as providing meaningful diversification, improving a portfolio’s efficiency by reducing volatility without necessarily sacrificing returns.

Private real estate has demonstrated this diversifying power through multiple market shocks. During the 2000–2002 Dot-Com Crash, private real estate delivered positive income as equities fell sharply. In the 2008–2009 Global Financial Crisis, it declined but far less dramatically than public markets. And during the 2022–2023 rate shock, appraisal-based valuations helped cushion volatility while public equities and bonds experienced sharp drawdowns.

For investors seeking smoother return streams, reduced portfolio volatility, and better long-term compounding, private real estate’s low correlations make it an essential and stabilizing allocation.

Consistent Income Distribution

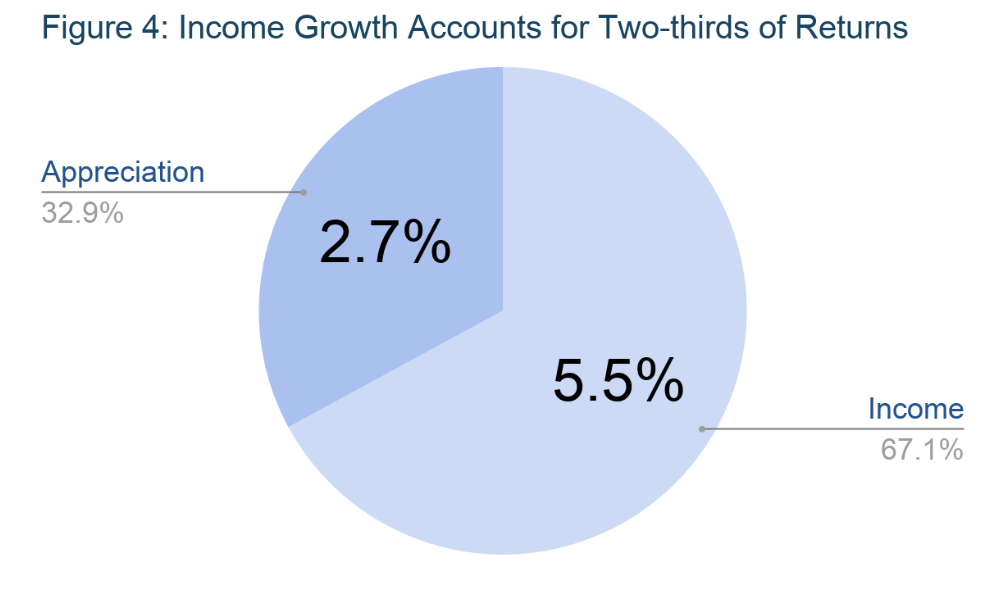

A defining characteristic of private real estate is its ability to generate steady, predictable income across cycles. Over the 20-year period from 2000 to 2020, NCREIF’s equity fund NFI-ODCE Index delivered an average annual total return of 8.1%, with volatility materially lower than equity dividends. A subsequent report puts that figure at 8.2%.

Source: Florida State Board of Administration

About two-thirds (5.5%) of that return is due to income, with appreciation accounting for (one-third) 2.7%.

Importantly, income growth over this period has generally tracked or exceeded inflation, supported by steady increases in net operating income (NOI).

This stability is rooted in real estate’s structural features. Long-term leases, typically running 3–10 years, provide durable cash flows. Contractual rent escalations, often tied to CPI or fixed annual bumps, help maintain real income in inflationary environments. Triple-net lease structures, which shift operating costs to tenants, further strengthen predictability. Meanwhile, broad geographic and tenant diversification reduces reliance on any single industry or market.

Unlike dividends, which corporations can reduce or suspend during downturns, rental obligations persist contractually, providing a more resilient income stream. This is especially valuable during periods of market stress.

For family offices and long-horizon investors seeking stable cash flow with inflation protection, private real estate’s consistent income distribution is a foundational pillar of its appeal.

Potential Inflation Hedge

Private real estate has long been viewed as a potential hedge against inflation, and the historical data supports this perception.

NCREIF data show that commercial real estate NOI growth has been positively related to inflation over multiple decades, with one study finding a correlation of roughly 0.5 between NPI NOI growth and CPI from 1978–2011. More recent work from Goldman Sachs notes that NPI Net Operating Income (NOI) has consistently outpaced inflation over the long term, underscoring private real estate’s role as an income-based inflation hedge.

Several mechanisms explain this inflation-responsive behavior. Contractual rent escalations, often tied to CPI or fixed annual increases, help maintain purchasing power during inflationary periods. When leases expire, market rent resets allow landlords to capture prevailing rental rates, a critical feature in fast-rising environments.

Operating expense pass-throughs shift costs such as taxes, insurance, and utilities to tenants, preserving margins. Meanwhile, rising replacement costs for construction and materials provide valuation support, reinforcing the economic rationale for higher rents. Lastly, as real assets, properties benefit from the intrinsic value of land and physical structures, which tend to appreciate alongside general price levels.

It is important to note, however, that real estate is not a perfect or immediate inflation hedge. Longer leases can introduce lag effects before rents adjust to new price conditions. With inflation still running above the Federal Reserve’s 2% target in 2026, the role of private real estate as a long-term inflation hedge remains especially relevant for investors seeking durable, purchasing-power-protected returns.

The Shoora Capital Approach

Shoora Capital brings an institutional mindset to the middle market while preserving the agility and accountability of a principal-led investment firm. Our approach is built on serving as a bridge between high-quality local operators and sophisticated investors, creating aligned partnerships that unlock opportunities often overlooked by large institutions.

By investing our own capital alongside clients, we maintain direct accountability, reinforcing disciplined underwriting and long-term value creation. Central to that discipline is strict basis control at entry and conservative leverage designed to preserve downside protection before upside optimization.

Shoora Capital sources transactions primarily through established operator relationships within targeted Sunbelt submarkets, supplemented selectively by brokered processes where recapitalizations, estate-driven sales, or capital stack resets create pricing inefficiencies.

A meaningful portion of deal flow comes from repeat sponsors operating within defined geographic niches, allowing for information continuity, operating transparency, and faster underwriting cycles. We avoid broadly intermediated auctions where pricing is driven primarily by leverage expansion or cap rate compression assumptions.

Underwriting discipline is structured around defined guardrails. Target loan-to-value ratios typically range between 55% and 65%, with stressed debt service coverage ratios modeled at or above 1.30x under downside rent and occupancy scenarios. Exit cap rates are underwritten with expansion of 50–100 basis points relative to entry assumptions, depending on asset class and submarket liquidity.

Rent growth projections are based on trailing 10-year submarket averages rather than peak-cycle comparables. Capital expenditure scopes are fully defined at acquisition, with contingency reserves generally ranging from 5–10% of planned project costs. We underwrite for durability: stabilized yield on cost, DSCR resilience under rate expansion, and refinancing feasibility without relying on aggressive valuation assumptions.

Post-acquisition, value creation is operational and measurable. Revenue management focuses on mark-to-market leasing, unit renovation programs supported by rent elasticity analysis, and ancillary income optimization where tenant demand supports it. Expense management includes vendor contract renegotiation, property tax appeal strategies, insurance restructuring where appropriate, and utility efficiency initiatives.

Capital improvements are phased and tied to defined return thresholds rather than cosmetic repositioning. Asset-level reporting tracks NOI margins, rent spreads, leasing velocity, and budget variance monthly. Financing strategy prioritizes duration alignment and interest rate risk management. Projected returns are not dependent on cap rate compression at exit.

Conclusion

Private real estate offers a rare combination of characteristics that make it a cornerstone of long-term, multi-asset portfolios. Over certain historical periods, private real estate has delivered competitive returns with lower reported volatility than many public market real estate benchmarks. With low correlations to equities and fixed income, private real estate enhances overall portfolio diversification and helps smooth return patterns when public markets become volatile.

Its consistent income generation, supported by durable leases and diversified tenant bases, provides a reliable source of cash-flow, while its sensitivity to inflation enables real estate to help preserve purchasing power over time. Underpinning all of this is the security of a tangible, productive asset, viz. land and buildings that serve essential economic functions.

These strengths explain why leading institutions, pensions, endowments, and sovereign wealth funds have long maintained 10–15% strategic allocations to private real estate. Yet family offices and individual investors remain significantly under-allocated, often holding less than a quarter of the exposure found in institutional portfolios.

If you are evaluating a strategic allocation to private real estate, we invite you to review our current investment themes and underwriting framework. Request the investor deck or speak directly with our team to discuss how disciplined basis selection and conservative leverage are applied in today’s market environment.

Frequently Asked Questions

How liquid is private real estate?

Private real estate is generally considered a long-term, illiquid investment. Unlike publicly traded REITs, interests in private funds or direct properties are not bought and sold daily on an exchange. Liquidity, if available, is typically governed by fund structures, redemption windows, or asset sale timelines. Investors should be prepared to commit capital for multiple years.

How are private real estate valuations determined?

Valuations are typically based on periodic third-party appraisals, comparable transactions, and discounted cash flow analysis rather than continuous market pricing. This appraisal-based framework can produce smoother reported returns but may introduce timing lags during periods of rapid market repricing.

What is the typical investment timeline?

Private real estate investments commonly operate on a 3–7 year hold period, depending on strategy (core, value-add, opportunistic, or development). Core strategies often emphasize long-term income stability, while value-add and opportunistic strategies may target defined operational or repositioning timelines before exit.

Who is private real estate generally suited for?

Private real estate is typically appropriate for investors with a long-term investment horizon, tolerance for limited liquidity, and a desire for income generation and portfolio diversification. It is often utilized by pensions, endowments, family offices, and accredited investors seeking durable, risk-adjusted returns.

How does private real estate fit within a broader portfolio?

Institutions frequently maintain a 10–15% strategic allocation to real estate as part of a diversified multi-asset portfolio. Private real estate may enhance diversification due to historically low correlations with equities and bonds, while also contributing contractual income that can support portfolio stability across market cycles. Disclaimer: This content is for educational and informational purposes only and should not be construed as investment advice. Real estate investments involve risk, including potential loss of principal. Past performance does not guarantee future results. Consult with qualified financial, legal, and tax professionals before making investment decisions.